Unit Rate Pricing in Estimating

What Is a Unit Rate?

A unit rate is the total cost of carrying out one unit of a specific item of construction work. If a bill of quantities includes an item for “in-situ concrete in foundations, C25 designated mix,” measured in cubic metres, the unit rate is the all-in cost to the contractor of placing one cubic metre of that concrete — covering labour, materials, plant, overheads, and profit.

Unit rate pricing is the engine of construction estimating. Every line item in a bill of quantities is priced using a unit rate. Those rates, multiplied by the measured quantities, produce the contract sum. The same rates are then used throughout the project to value work for interim payments, price variations, and settle final accounts. Getting unit rates right — or understanding where a contractor’s rates are wrong — is one of the most fundamental skills a quantity surveyor can develop.

The Components of a Unit Rate

A properly built unit rate is assembled from first principles, working from the bottom up. There are five main components.

Labour is the cost of the operatives who carry out the work. This is not simply their basic hourly wage — it is the all-in rate, which includes employer’s National Insurance, holiday pay, pension contributions, CITB levy, sick pay, tool allowances, travel, and recruitment costs. A basic wage of £16.50 per hour typically becomes an all-in cost of £23–£24 per hour once all statutory and contractual additions are included — a 40% uplift that catches out anyone pricing from basic wages alone.

Labour is priced by gang, not by individual. A bricklaying gang might consist of one bricklayer and one labourer. A concrete gang might be three labourers and a foreman. The gang cost per hour, divided by the expected output (how many units the gang can complete per hour or per day), gives the labour cost per unit.

Materials include the supply cost of everything consumed in the work — bricks, concrete, mortar, reinforcement, fixings, sealants — plus delivery to site, unloading, storage, and a waste allowance. Waste is unavoidable in construction: bricks break during handling (allow 5–7%), timber generates offcuts (10–12%), concrete spills and is over-ordered (5%), and plasterboard suffers cutting losses (10–15%). Failing to include waste means the rate will not cover the actual material consumed.

Plant covers the equipment and machinery needed to carry out the work — from a concrete pump for foundation pours to scaffolding for brickwork at height. Plant costs include hire rates, fuel, operator costs (if separate from hire), and mobilisation and demobilisation. Some plant is allocated to specific unit rates (a concrete pump spread across the cubic metres of concrete placed), while major items like tower cranes are typically carried in the preliminaries.

Overheads cover two categories. Site overheads (preliminaries) include site management, welfare facilities, insurances, security, and temporary works — typically 35–50% of direct labour cost. Head office overheads cover the contractor’s central administration, estimating department, accounts, and business costs — typically 10–18% of direct costs. Both must be recovered through the rates priced in the bill.

Profit is the contractor’s margin after all costs are covered. In UK construction, main contractor margins typically range from 3–5% on competitive tenders, while specialist subcontractors may target 5–10%. The margin varies with market conditions, project risk, and the contractor’s appetite for the work.

Building an All-In Labour Rate

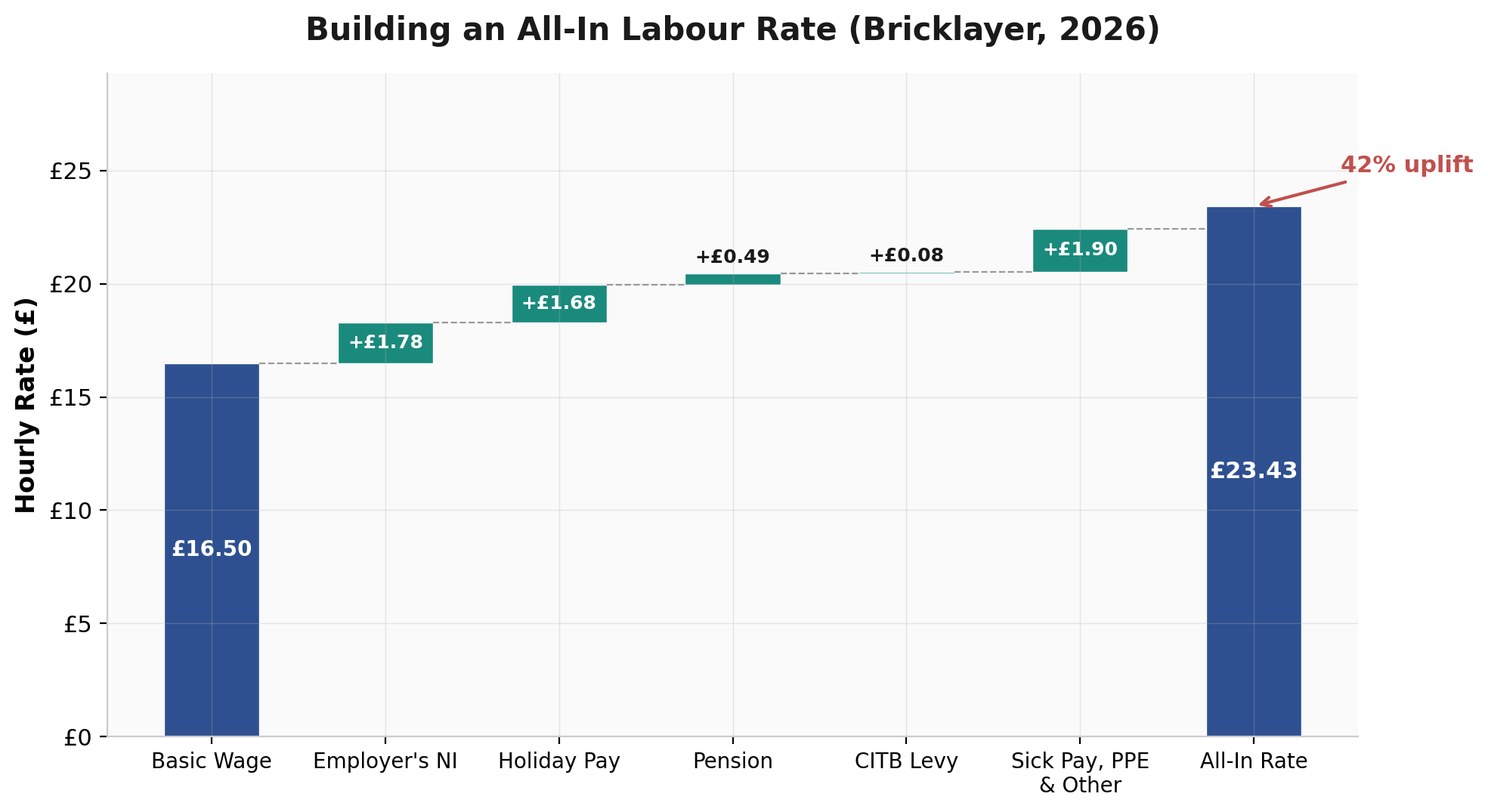

The all-in labour rate is one of the most important calculations in estimating — and one of the most commonly misunderstood. Here is how it works for a qualified bricklayer in 2026.

Start with the basic hourly wage: £16.50. Then add each statutory and contractual cost the employer must bear on top of that wage.

Employer’s National Insurance is payable at 15% on earnings above the annual threshold (currently around £9,100). For an operative earning £32,175 per year (37.5 hours × 52 weeks × £16.50), this adds approximately £1.78 per hour.

Holiday pay adds a further loading. Construction workers are entitled to 4.8 weeks of paid holiday per year. Since the operative is paid during holidays but not producing output, this cost must be spread across the working weeks. Rolled up into the hourly rate, it adds approximately £1.68 per hour.

Pension contributions under auto-enrolment require a minimum 3% employer contribution, adding around £0.49 per hour. The CITB levy (0.5% of payroll for larger employers) adds £0.08 per hour. Sick pay provision, tool and PPE allowances, travel allowances, and recruitment and administration costs collectively add a further £1.90 per hour.

The result: a basic wage of £16.50 becomes an all-in rate of approximately £23.43 per hour — before any allocation for site supervision or overheads. That 42% uplift is the difference between pricing a job correctly and losing money on every hour worked.

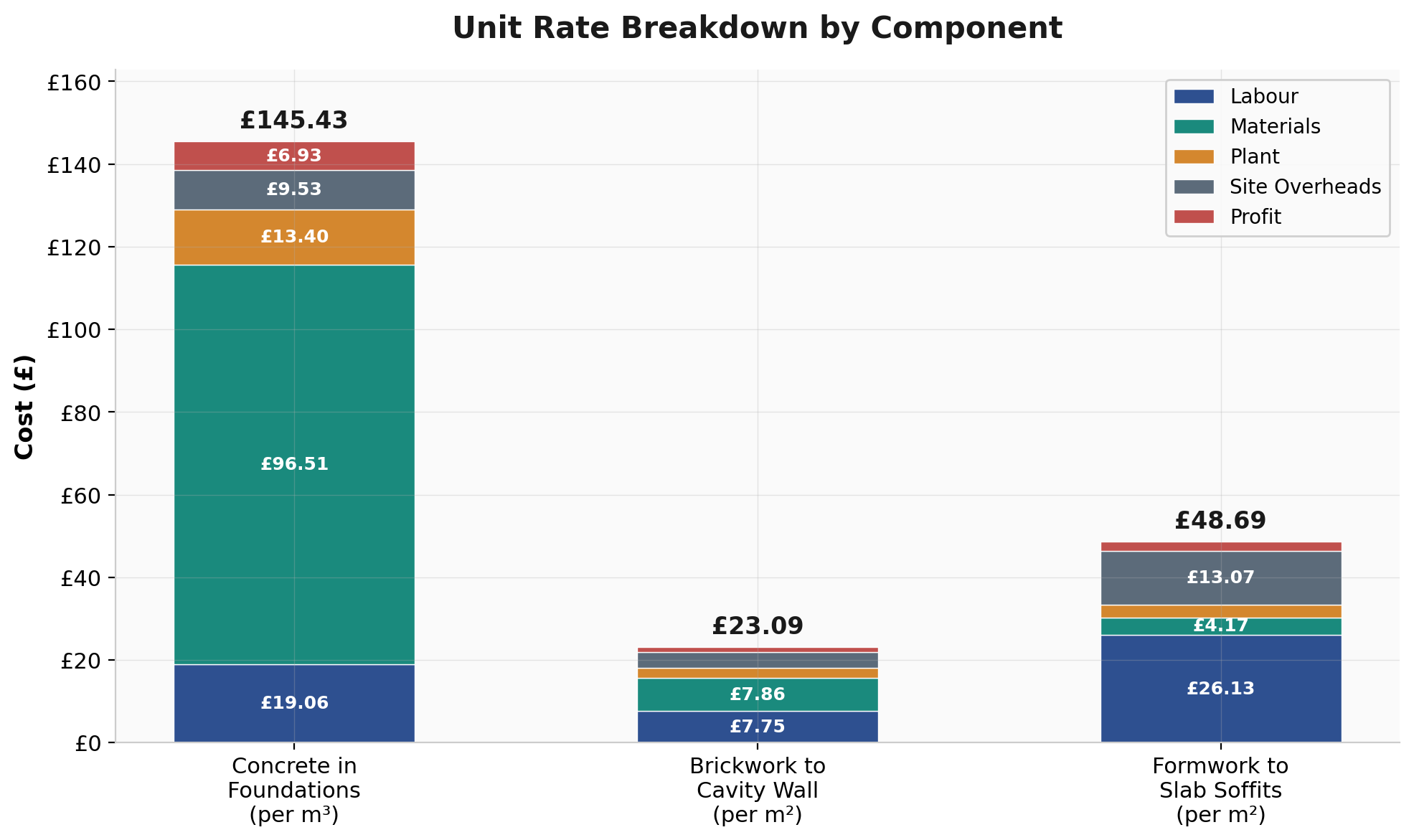

Worked Example: Concrete in Foundations

To see how the components come together, consider a unit rate for placing C25 ready-mix concrete in foundations, measured per cubic metre. This example assumes good site access, a 50 m³ pour, and standard conditions.

Labour: A gang of four (one foreman at £25.00/hour plus three labourers at £23.43/hour) costs £95.29 per hour. At an output of 40 m³ per day (eight hours), the gang places 5 m³ per hour. Labour cost = £95.29 ÷ 5 = £19.06 per m³.

Materials: Ready-mix C25 concrete delivered to site costs around £85–£86 per m³. Add fabric reinforcement (approximately £1.91/m³ for A393 mesh in a slab), admixtures (£4/m³), and a 5% waste allowance on all materials. Materials total = approximately £96.51 per m³.

Plant: A concrete pump at £120 per day plus setup costs, spread across the pour volume, adds around £6.40/m³. Edge formwork hire and installation adds another £7.00/m³. Plant total = £13.40 per m³.

Site overheads: Allocated as a percentage of labour (50%), this adds £9.53 per m³.

Profit: At 5% on all direct costs, this adds £6.93 per m³.

Total unit rate: £145.43 per m³. This sits comfortably within the typical UK range of £130–£160/m³ for standard foundation concrete in good conditions. Poor access, confined working, or small quantities would push the rate higher. For a detailed breakdown of what goes into measuring concrete works, see our dedicated article on the subject.

Worked Example: Brickwork to Cavity Wall

Now consider a unit rate for the outer skin of a cavity wall in standard clay facing bricks, measured per square metre. This assumes ground floor work up to 4m, good access, and straightforward bonding.

Labour: A gang of one bricklayer (£25.00/hour) and one labourer (£23.43/hour) costs £48.43 per hour. At an output of approximately 50 m² per day (roughly 500 bricks at 10 bricks per square metre), labour cost = (£48.43 × 8) ÷ 50 = £7.75 per m².

Materials: Facing bricks at £0.32 each (10 per m²) = £3.20. Mortar at 0.06 m³ per m² at £65/m³ = £3.90. Cavity wall ties at £0.30/m². Add a waste allowance (3% on bricks, 5% on mortar) = £0.46. Materials total = approximately £7.86 per m² (excluding DPC, which is often measured separately).

Plant: Scaffold hire at £2.50/m² per week, spread across the brickwork output for that section, contributes around £2.00/m². A mortar mixer adds roughly £0.50/m². Plant total = £2.50 per m².

Site overheads: At 50% of labour = £3.88 per m².

Profit: At 5% = £1.10 per m².

Total unit rate: approximately £23.09 per m² for the brick skin alone. This is a realistic rate for standard conditions; restricted access, complex bonding patterns, or work at height would all increase the labour and plant components.

Worked Example: Formwork to Slab Soffits

Formwork is an interesting example because the materials (plywood, timber bearers, props) are reused multiple times, and the number of uses directly affects the unit rate.

Labour: A formwork gang of two carpenters (£24.50/hour each) costs £49.00 per hour. At an output of 15 m² of soffit formwork erected per day, labour cost = (£49.00 × 8) ÷ 15 = £26.13 per m².

Materials: Plywood facing at £25 per sheet (covers approximately 2.88 m²) = £8.68/m² new. If the plywood achieves four uses, the cost per use = £8.68 ÷ 4 = £2.17. Timber bearers and supports add £1.50/m² per use. Nails, release agent, and sundries = £0.50/m². Materials total = approximately £4.17 per m².

Plant: Adjustable steel props (Acrow props) at hire rates spread across the formwork area add approximately £3.00 per m².

Site overheads: At 50% of labour = £13.07 per m².

Profit: At 5% = £2.32 per m².

Total unit rate: approximately £48.69 per m². The key variable here is the number of plywood uses. If the formwork only achieves two uses (due to damage or complex shapes), the materials component nearly doubles. If it achieves six uses on a repetitive floor plate, it drops significantly. This is why formwork costs vary so widely between projects — and why the QS must understand what is driving the rate.

Pricing Methods

There are two broad approaches to arriving at unit rates, and most estimators use a combination of both.

First principles estimating builds every rate from scratch, as shown in the examples above. The estimator calculates the labour, materials, plant, and overheads for each item based on current market prices, expected productivity, and project-specific conditions. This is the most accurate approach but also the most time-consuming. It is essential for large or unusual projects where published rates may not reflect the actual conditions.

Price book estimating uses published rate guides — such as Spon’s Price Books, Laxton’s, or BCIS cost data — as the starting point. These publications provide benchmark unit rates for standard items, updated annually. The estimator adjusts published rates for location (using BCIS location factors), project complexity, market conditions, and any project-specific requirements. Price books are faster to use but carry the risk of applying generic rates to non-standard situations.

In practice, experienced estimators use first principles for the major cost items (concrete, structural steel, cladding, M&E) and price books for minor or standard items where the effort of a full build-up is not justified. The QS reviewing a tender should be able to identify which approach the contractor has used — and challenge rates that look either unrealistically low (risk of claims later) or unnecessarily high.

Unit Rates Through the Project Lifecycle

Unit rates are not just a tendering tool. They appear at every stage of a construction project.

During cost planning, the QS uses elemental unit rates — cost per square metre of gross internal floor area, or cost per unit of a functional element — to build early-stage estimates before detailed design is available. BCIS provides benchmark elemental rates drawn from actual project data, adjusted for location and date.

During tendering, the contractor’s estimator prices every item in the BOQ using unit rates built from first principles, price books, or subcontractor quotations. The priced BOQ becomes the contract sum and the basis for all subsequent financial management.

During construction, the contract unit rates are applied to measured quantities of completed work to produce interim valuations. If the employer instructs a variation — additional work or a change to the specification — the existing contract rates are used as the starting point for pricing the variation. Where the variation is of a similar character and executed under similar conditions, the contract rates apply directly. Where the character or conditions differ significantly, new rates are negotiated, often built from first principles.

During post-contract cost management and final account settlement, unit rates are scrutinised closely. Disputes frequently arise over whether a contract rate fairly reflects the work carried out — particularly where conditions on site differed from those assumed at tender stage.

Common Pitfalls

Using basic wages instead of all-in rates. As shown above, the all-in labour cost is 40% or more above the basic wage. Pricing from basic wages alone means the contractor loses money on every hour worked — a mistake that compounds rapidly across a project.

Ignoring or underestimating waste. Every material has a waste factor, and it varies by material type. Pricing bricks at net quantity without a 5–7% waste allowance, or concrete without 5% for spillage and over-ordering, produces rates that cannot cover the actual material consumed on site.

Assuming standard productivity. Published output rates assume reasonable working conditions — good access, adequate space, competent operatives, fair weather. In reality, productivity is affected by site congestion, weather delays, working at height or in confined spaces, learning curves for new teams, and cumulative fatigue over long programmes. A bricklayer who lays 500 bricks per day on a clear site may manage only 350 in a congested, multi-storey project with scaffold moves and material handling constraints.

Not updating historic rates. A rate that was competitive two years ago may be significantly below current market prices. Material costs fluctuate, labour rates increase annually, and plant hire costs respond to demand. The QS should always adjust historic rates for inflation — the RICS Building Cost Index provides a reliable basis for doing so.

Confusing net and gross rates. A net rate covers the direct cost of labour, materials, and plant for the work item. A gross rate also includes site overheads and profit. Double-counting overheads (including them in both the unit rate and the preliminaries section) inflates the tender; omitting them from both means they are never recovered.

Treating all work as standard. Work in restricted areas, at height, in occupied buildings, or in specialist environments (clean rooms, laboratories, hospitals) takes longer and costs more than equivalent work in open, clear conditions. The estimator must adjust output rates and allow for additional plant and safety measures. The QS reviewing a tender should check whether the contractor has made these adjustments — especially where the specification or site conditions are unusual.

Getting Unit Rate Pricing Right

Unit rate pricing sits at the heart of quantity surveying practice. Whether you are building rates from first principles for a tender, reviewing a contractor’s priced bill for reasonableness, valuing completed work for an interim certificate, or negotiating variation rates on a live project, the ability to understand what goes into a rate — and spot where something has been missed or mispriced — is essential.

The worked examples in this article show the mechanics. In practice, every project brings its own conditions, and professional judgement is always needed to adjust rates for the specific circumstances. But the principles are consistent: identify the labour, materials, and plant required; account for waste, productivity, and overheads; add a realistic margin for profit; and check the result against market benchmarks. That discipline, applied rigorously, is what separates accurate estimating from guesswork.

Further Reading

BCIS: Building Cost Information Service — Industry-standard cost data, elemental rates, and location factors for UK construction estimating and cost planning.

Spon’s Price Books — Annual published rate guides covering architects’ and builders’, civil engineering, mechanical and electrical, and external works pricing.

RICS Building Cost Index — Monthly index tracking construction cost movements in the UK, essential for updating historic rates for inflation.

CITB: Construction Industry Training Board — Information on construction skills, training levies, and labour cost benchmarks for the UK construction industry.

CIOB: Construction Estimating and Cost Management CPD — Professional development resources on estimating practice, cost control, and commercial management from the Chartered Institute of Building.